Rental Property Sale Capital Gains: A 2026 Tax Guide

You accept the offer. Then the second thought hits you.

Not, “Did I price it right?”

It's, “How much of this am I keeping after taxes?”

That question catches a lot of landlords off guard, especially if you're selling fast. Maybe the tenant moved out, repairs are piling up, or you just want a clean exit instead of another year of vacancy, maintenance calls, and uncertainty. The sale part can be simple. The tax part usually isn't.

Most owners start with a rough mental formula: sale price minus what I paid. For a rental, that shortcut often misses the biggest surprises. Your final tax picture can include more than one moving part, and one of the most overlooked pieces is depreciation recapture. That's the line item that makes many landlords say, “Wait, why am I paying tax on that too?”

If the property also ties into inheritance, probate, or co-ownership questions, legal structure matters alongside tax planning. For readers dealing with shared ownership issues, this explainer on estate planning for Ontario property owners can help frame how title decisions affect what happens next.

A sale also gets more complicated if the property is still occupied or actively marketed. If that's your situation, this guide on renting a house that is for sale covers some of the practical landlord issues that come up before closing.

Your Guide to Rental Property Sale Taxes

You accept an offer because you want a simple exit. Then the key question shows up fast: how much cash do you keep after closing?

For a rental property, the answer is rarely just sale price minus what you paid. The tax bill works like a receipt with separate line items. One line may be long-term capital gain. Another may be depreciation recapture, which is the part many landlords miss until it cuts into proceeds. Then comes the decision piece: take the cash sale, try a 1031 exchange to defer taxes, or use a different strategy if the timing and your goals allow it.

If you are selling while the property is still occupied, the logistics can affect your timeline and your options. This practical guide to renting a house that is for sale can help you sort out that side before closing.

The three ideas that shape your result

Holding period affects how the gain is taxed. For 2026, a property held more than one year is generally in long-term capital gain territory. A property held one year or less is generally taxed at ordinary income rates, which can change the math in a hurry.

Your taxable gain is based on adjusted basis, not just purchase price. That means the IRS starts with what you paid, then adjusts for items such as depreciation and certain improvements. Many landlords expect tax only on appreciation. The calculation is usually less forgiving than that.

A simple exit and a low tax bill are not always the same choice. A fast cash sale can be the right move if you want certainty, fewer repairs, and no more landlord headaches. A 1031 exchange can defer part of the tax cost, but it also keeps you in the investment cycle and comes with rules, deadlines, and replacement property pressure. If your top priority is being done, that tradeoff matters.

Here is the part that surprises many sellers. Depreciation recapture can create tax even when the sale feels modest. You took depreciation deductions over the years, and those deductions lowered your basis. On sale, the IRS wants to account for that benefit. In plain English, part of your tax bill may come from prior write-offs, not just from market appreciation.

That is why two landlords can sell at similar prices and walk away with very different net proceeds.

A quick decision framework helps. If you want cash, speed, and closure, estimate the after-tax proceeds of a straight sale first. If the tax hit feels too large and you still want real estate exposure, examine whether a 1031 exchange fits your timeline and risk tolerance. If family ownership, inheritance, or title questions are involved, legal structure can affect the best path, and this explainer on estate planning for Ontario property owners may help frame those issues.

Practical rule: judge the offer by what lands in your account after taxes, not by the headline sale price alone.

Breaking Down Your Tax Bill Components

Closing day can feel simple. Money comes in, mortgage gets paid off, and you expect one final tax number. In practice, the IRS treats your sale more like a receipt with separate charges listed on different lines.

That distinction matters if you want a quick, clean exit. A cash offer may solve the selling side fast, but your bottom line still depends on which tax buckets apply and how large each one is.

Capital gains tax

One part of the bill is capital gains tax. This applies to the gain created when you sell the property for more than its adjusted basis.

Holding period affects how that gain is taxed. For 2026, long-term capital gains generally apply when you held the property for more than one year, while short-term treatment generally applies when you held it for one year or less. Long-term rates are usually lower than ordinary income tax rates, which is why ownership length can change the result even when two landlords sell for similar profits.

That is one reason the sale price alone never tells the whole story.

Depreciation recapture tax

The second part is often the surprise. Depreciation recapture is the tax issue tied to the depreciation deductions you claimed while the property was a rental.

A simple way to view it is this: your tax bill works like a receipt with multiple line items. One line covers appreciation. Another line covers deductions you already received through depreciation. You may feel like you have one gain, but the tax return can divide that gain into separate pieces.

For landlords who want a simple exit, this is the line item to watch closely. A property may not have exploded in value, yet the recapture piece can still create a meaningful tax cost because years of depreciation reduced your basis.

Why sellers get tripped up

Confusion usually starts because three different numbers sound like they should mean the same thing. They do not.

| Tax concept | What it refers to | Why sellers confuse it |

|---|---|---|

| Sale profit | The overall economic gain from the transaction | It feels like one number should determine the whole outcome |

| Capital gain | The tax category tied to gain and holding period | Many landlords assume this is the only tax issue |

| Depreciation recapture | The tax result tied to prior depreciation deductions | Many owners do not realize past write-offs can affect the sale |

A landlord who wants speed and closure should read this table almost like a decision tool. If the recapture amount is small, a straight sale may be easy to justify. If the recapture and gain together create a large tax bite, that is when it may be worth comparing a 1031 exchange or other planning options before you sign.

The key point is simple. Your tax bill is rarely one bucket. It is usually a few line items added together, and depreciation recapture is often the one that changes the final number more than expected.

How to Calculate Your Taxable Gain

The core formula is simple. The hard part is using the right starting number.

For a rental property sale, the taxable gain is generally computed as sale price minus adjusted basis, and adjusted basis starts with your purchase price, is increased by capital improvements, and reduced by depreciation, as explained in this rental property capital gains overview from 1800Accountant.

Start with adjusted basis

Most landlords remember what they paid. Fewer have a clean number for adjusted basis.

That number usually starts with the original purchase price. Then you adjust it over time.

A plain-English version looks like this:

| Step | What happens |

|---|---|

| Begin | Start with what you paid for the property |

| Add | Include capital improvements that increase basis |

| Subtract | Reduce basis by depreciation claimed over time |

That final number is what the IRS compares to your sale side of the transaction.

What counts as an adjustment

Not every dollar you spent on the property changes basis in the same way. A repair that kept the place running isn't always treated like a major improvement that added value or extended useful life.

For practical planning, many landlords sort their paperwork into three piles:

- Purchase documents: Settlement statement, deed records, loan closing paperwork

- Improvement records: Roof replacement, major renovation, room addition, system upgrades

- Depreciation records: Tax returns and depreciation schedules

If one of those piles is missing, the tax estimate gets fuzzy fast.

Why depreciation changes everything

This is the part that surprises people.

Depreciation helped reduce taxable rental income while you owned the property. But because those deductions reduced basis, they also increase the gain recognized when you sell if everything else stays equal.

Basis is like the property's tax book value. Each depreciation deduction writes that number down. So when you eventually sell, the gap between sale price and basis can be larger than you expected.

Keep this in mind: A landlord can feel like the property only “went up a bit,” but the tax calculation can still show a larger gain because basis has been reduced over time.

A clean worksheet approach

If you're trying to estimate your own rental property sale capital gains before talking to a CPA, use a worksheet in this order:

- Write down the sale price

- Gather selling costs

- Find original purchase records

- Add documented capital improvements

- Pull depreciation schedules from prior returns

- Calculate adjusted basis

- Estimate gain before deciding whether to sell now, defer, or wait

Many quick-sale decisions gain clarity. Once you know your likely taxable gain, you can compare a fast close against holding longer, exchanging, or changing the timing.

A Real-World Sale Calculation Example

Numbers make this easier, so let's walk through a fictional example.

Sarah bought a rental years ago and now wants out. The tenant has moved, the property needs work, and a cash buyer makes the process simple. Her first question isn't whether she can sell. It's what the sale means after taxes.

A common blind spot in consumer content is depreciation recapture. Many articles focus on the headline capital gains rate and skip the separate tax impact created by depreciation deductions, as noted in Rocket Mortgage's discussion of capital gains on rental property.

Sarah's sale numbers

We'll use a simple fact pattern to show the mechanics.

| Item | Calculation | Amount |

|---|---|---|

| Purchase price | Original cost | $300,000 |

| Capital improvement | New roof | $20,000 |

| Less depreciation claimed | Reduces basis | $80,000 |

| Adjusted basis | $300,000 + $20,000 – $80,000 | $240,000 |

| Sale price | Cash buyer purchase | $500,000 |

| Closing costs | Selling expense | $20,000 |

| Net amount realized | $500,000 – $20,000 | $480,000 |

| Total gain | $480,000 – $240,000 | $240,000 |

Splitting the gain into buckets

Here's the part landlords need to see clearly.

Sarah's total gain is $240,000. But that total doesn't all sit in one tax bucket.

Because she claimed $80,000 of depreciation during ownership, that portion is the first place her tax preparer will focus when looking at depreciation recapture. The remaining $160,000 is the gain left after separating that depreciation-related piece.

This is why the final tax result can feel counterintuitive. Sarah may have thought, “I made money, so I'll just owe long-term capital gains tax.” In reality, the tax receipt can have one line tied to depreciation history and another tied to the remaining gain.

If you've owned a rental for a long time, depreciation recapture often matters just as much as the headline capital gains rate.

Why this example matters

Sarah's story is ordinary. That's exactly why it's useful.

She didn't use an exotic tax strategy. She owned a rental, improved it, depreciated it, and sold it. That's enough to create a tax picture that's more layered than most sellers expect.

If your own records look messy, don't guess. Rebuild the file before closing so you know what part of your gain comes from appreciation and what part comes from prior depreciation.

Strategies to Reduce or Defer Your Tax Bill

Once you understand the gain calculation, the next question is practical: what should you do about it?

For many landlords, the primary choice isn't “How do I avoid tax entirely?” It's “Which path fits the life I want after this sale?”

The simple-exit decision framework

Start with three questions:

- Do you want cash now? If yes, a straight sale may fit better than a reinvestment strategy.

- Do you want another property? If no, a 1031 exchange may add complexity without helping your actual goal.

- Can timing help? Some sellers can benefit by closing in a lower-income year or offsetting gains with losses.

A key seller decision is whether to sell, use a 1031 exchange, or wait for a lower-income year. The best path depends on current interest rates, replacement-property economics, and whether you want liquidity now versus future tax deferral, as discussed in SmartAsset's guide to reducing capital gains tax on rental property.

Here's a quick visual overview before we compare the options in plain language.

Option one, the 1031 exchange

This route is for landlords who still want real estate exposure.

A 1031 exchange defers tax by moving proceeds into another qualifying investment property. The key word is defer. It doesn't erase the tax. It pushes it forward.

This can work well for someone who wants to keep building a portfolio, shift markets, or move from a management-heavy rental into something simpler. It's usually a poor fit for the owner who is done being a landlord and wants a clean exit.

Option two, the primary residence exclusion

This one is powerful, but many rental owners assume it applies when it doesn't.

The main U.S. home-sale exclusion allows up to $250,000 of gain to be excluded for single filers and $500,000 for married couples filing jointly if the owner meets the 2-out-of-5-year ownership-and-use test. Investment and rental properties generally do not qualify unless they were used as a primary residence for the required period, according to this explanation of the home-sale exclusion rules.

If the property was purely a rental, don't assume this exclusion saves you.

Option three, installment sale or plain sale now

An installment sale spreads payments over time. That can spread recognition of gain over time as well. It may help a seller who doesn't need all proceeds immediately and is comfortable receiving payments instead of one lump sum.

But many landlords selling distressed, vacant, inherited, or management-heavy rentals want certainty, not a long tail of future collections. In those cases, a straightforward sale often matches the actual goal better.

That's where practical selling options matter. A direct buyer such as Cyber Homes purchases as-is for cash and closes on the seller's timeline, which can suit landlords who value speed and certainty over reinvestment complexity.

A side-by-side way to decide

| Strategy | Best fit | Main tradeoff |

|---|---|---|

| 1031 exchange | You want to stay invested in real estate | Defers tax, but keeps you in the property world |

| Primary residence exclusion | You truly meet the use and ownership rules | Often unavailable for a straight rental |

| Installment sale | You can accept payments over time | Less immediate liquidity and more ongoing risk |

| Straight cash sale | You want a simple exit and fast certainty | You may owe tax sooner instead of deferring it |

For readers who own commercial or mixed-use assets, Homebase's guide on CRE tax is a useful companion because it frames how tax planning can differ when the property isn't a standard single-family rental.

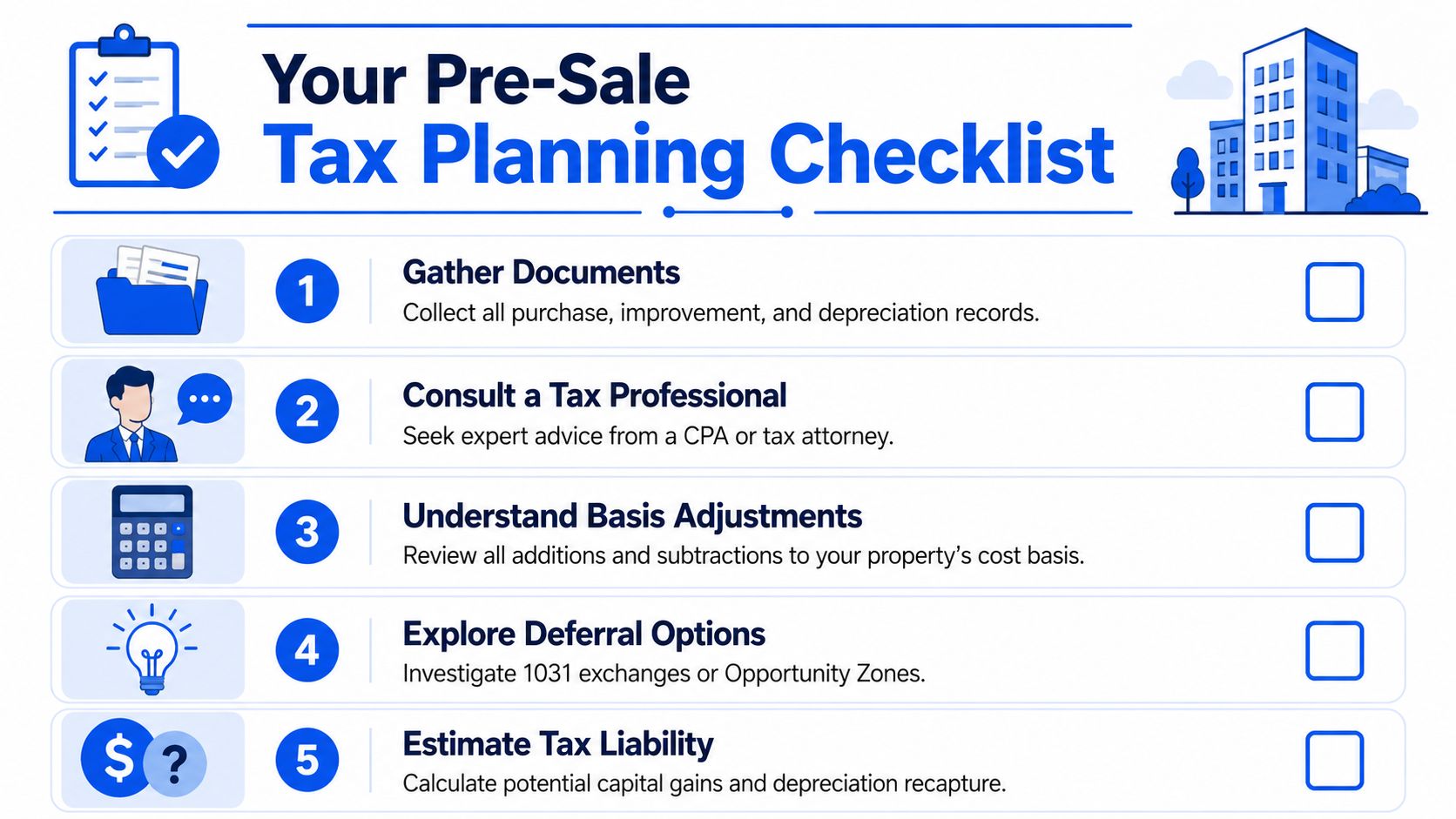

Your Pre-Sale Tax Planning Checklist

A quick sale doesn't leave much room for last-minute reconstruction. The smoother approach is to build your file before you sign final closing papers.

Documents to gather first

Get the paper trail together before you focus on strategy.

- Purchase records: Closing statement, deed, and any documents showing original acquisition cost

- Improvement file: Receipts, invoices, contractor agreements, and proof of payment for capital improvements

- Depreciation support: Prior tax returns and depreciation schedules

- Sale documents: Draft settlement statement, broker paperwork if applicable, and estimated closing costs

If you're still deciding whether to dispose of the property or keep it as a rental, this comparison on selling a home or renting it out can help clarify the bigger decision before you narrow down the tax path.

Questions to ask your tax professional

Don't just ask, “What will I owe?”

Ask better questions:

- How much of my gain is tied to depreciation history?

- Does my use of the property create any exclusion opportunity?

- Would a lower-income year change the outcome enough to wait?

- Does a 1031 exchange fit my goals, or just postpone a problem?

- What records do you need from me before closing?

Bring the depreciation schedules to the first meeting. Without them, many sale estimates are only rough guesses.

Your decision checklist

A key decision is whether to sell now, exchange, or wait for a lower-income year. The best answer depends on replacement-property economics, interest rates, and whether you want liquidity now or future tax deferral. Simple checklists often miss that tradeoff.

Use this final pre-sale screen:

| Checklist item | Why it matters |

|---|---|

| Know your basis | Basis drives the gain calculation |

| Confirm depreciation records | This is often where the surprise lives |

| Match strategy to life goals | Tax deferral isn't useful if you want out |

| Review timing | The year of sale can affect the final result |

| Get written estimates | Verbal guesses are easy to misremember |

Final Thoughts and Next Steps for a Smart Sale

Selling a rental can feel like a relief. It can also create a tax bill that's more layered than expected.

Three takeaways matter most. First, rental property sale capital gains aren't just “sale price minus purchase price.” Your adjusted basis changes over time. Second, depreciation recapture is often the hidden line item that changes the bottom line. Third, the right path depends on your real goal, not just the tax rule on paper. Some landlords want continued deferral. Others want a clean exit, cash, and no more property headaches.

If you're evaluating direct-sale options, it helps to understand how as-is home buyers typically fit into a fast-exit plan. The sale can be simple, but your tax prep still needs to be deliberate.

Bring your purchase documents, improvement records, depreciation schedules, and estimated closing statement to a qualified CPA or tax advisor before closing. A short meeting with organized records can save a lot of confusion and help you compare offers based on what you'll keep.

If you need to sell a rental quickly and want a straightforward cash option, Cyber Homes buys houses as-is and closes on your timeline. That can be useful when you're dealing with vacancy, repairs, probate, relocation, or just want a simple exit. Before you commit, pair the offer review with a tax estimate so you know your likely net proceeds, not just the sale price.