Sell Home or Rent It Out: Make the Right Choice in 2026

You're probably here because life moved first and you're trying to catch up.

A job transfer came through. You inherited a house you don't want to manage. A divorce, a probate timeline, or a second mortgage payment is forcing a decision faster than you'd like. On paper, the question looks simple: should you sell the house or keep it and rent it out?

It isn't simple.

This choice affects your cash, your taxes, your schedule, your stress level, and in some cases your credit and your ability to move on. That's why I don't treat this as a two-option decision. For many homeowners, there are three real paths: sell traditionally, rent it out, or take a fast cash sale and be done with it.

The Homeowner's Dilemma Sell Rent or Something Else

A lot of homeowners become accidental landlords without meaning to. They move for work, can't decide if prices will rise more, and think renting buys them time. Sometimes it does. Sometimes it just delays a hard decision and adds a second job.

This isn't a niche problem. After the housing crash, the U.S. ownership picture changed sharply. The national homeownership rate fell from 69.0% in 2004 to 63.7% in 2016, and during that same period Zillow reported that about 66% of sellers had considered renting before listing, as summarized by Great Lakes Real Estate's discussion of whether to sell or rent. That tells you something important: a huge share of sellers wrestle with this exact question before they act.

The mistake I see most often is treating the house like a spreadsheet only. It's not. A house can be an asset, but owning one from a distance or through a bad tenant can also become a constant drain on your time and judgment.

Practical rule: If keeping the property creates daily friction you already resent, don't assume rent checks will fix that feeling.

There are three honest paths:

- Sell traditionally: Best when the home shows well, you have time, and you want to maximize price.

- Rent it out: Best when cash flow is solid, you can tolerate landlord responsibilities, and you want to keep long-term exposure to the property.

- Take a fast cash sale: Best when speed, certainty, condition, or legal complexity matter more than stretching for top dollar.

The need isn't for more theory; it's for a clear filter. If you're trying to decide whether to sell home or rent it out, start with one blunt question: Do you want another investment property, or do you just want relief? Your answer usually points to the right path faster than any spreadsheet does.

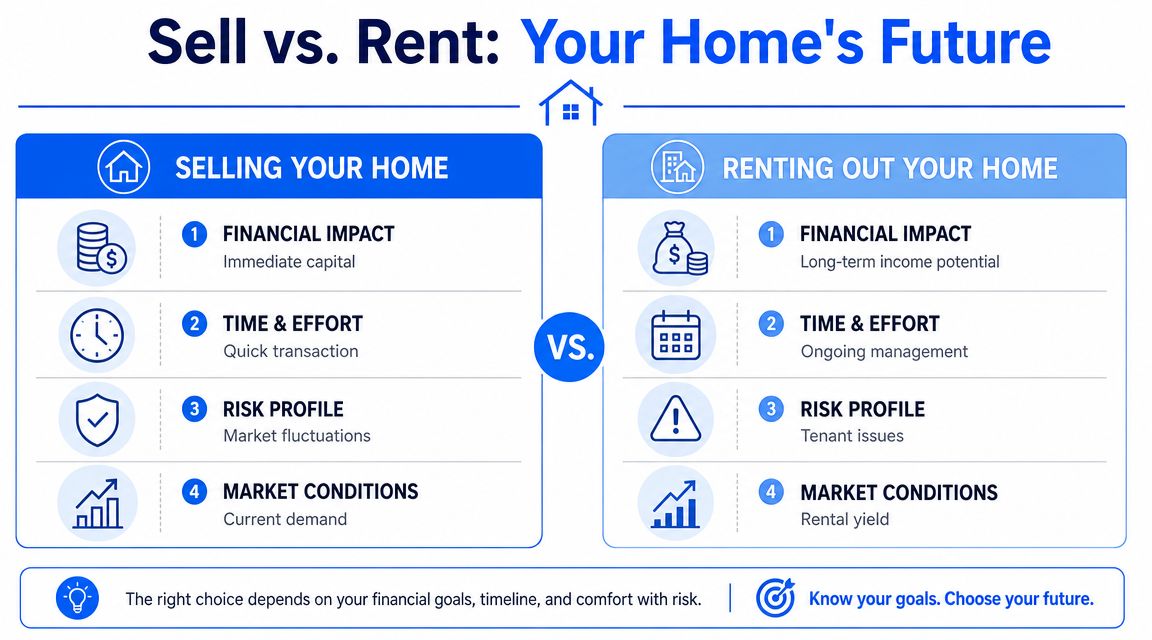

Comparing the Two Main Paths Selling vs Renting

The cleanest way to think about this is side by side. Selling and renting solve different problems.

| Decision area | Selling your home | Renting out your home |

|---|---|---|

| Financial outcome | Converts equity into a lump sum you can redeploy | Keeps you exposed to future upside and possible monthly cash flow |

| Time and effort | Intense for a short period, then it's over | Ongoing management, maintenance, leasing, and compliance |

| Risk exposure | You lock in a price and exit property risk | You keep market risk plus tenant and property risk |

| Lifestyle impact | Cleaner move, simpler finances, fewer loose ends | Ties you to the property and to landlord decisions |

Financial impact isn't just price versus rent

People often frame this as “sell for cash now” versus “collect rent later.” That's too shallow.

Selling gives you immediate liquidity. That matters if you need a down payment for the next home, want to pay off debt, or want one housing payment instead of two. Renting can build wealth, but only if the property performs after all expenses, not before.

If the property is occupied or you're dealing with a listing that overlaps with tenancy, the logistics get messy fast. That's why it helps to understand issues around renting a house that is for sale before you assume you can smoothly switch between strategies.

Time and effort separate owners from investors

Selling is a project. Renting is a business.

A traditional sale means prep work, showings, negotiation, and closing. Annoying, yes. Permanent, also yes. Renting means leases, repairs, collecting rent, dealing with turnover, and answering messages when something breaks at the worst possible time.

Here's a quick visual if you want the comparison in a more digestible format.

Risk sits in different places

Selling carries market-timing risk. You might wonder whether waiting would have produced a better price. But once you close, that risk is over.

Renting shifts the risk into operations. You're not just betting on appreciation. You're betting on tenant quality, repair costs, vacancy periods, legal compliance, and your own willingness to manage all of it.

Selling is cleaner. Renting can be richer. Cleaner and richer are not the same thing.

Lifestyle often decides it

If you're relocating, simplifying, settling an estate, or ending a chapter, selling usually fits the life event better. If you already think like an investor and you want to hold property long term, renting may fit.

The problem is that many homeowners choose based on emotion. They keep the house because they don't want to “lose” it. That's backward. Keep it only if the property serves your financial plan and your lifestyle. Nostalgia doesn't pay for a roof leak.

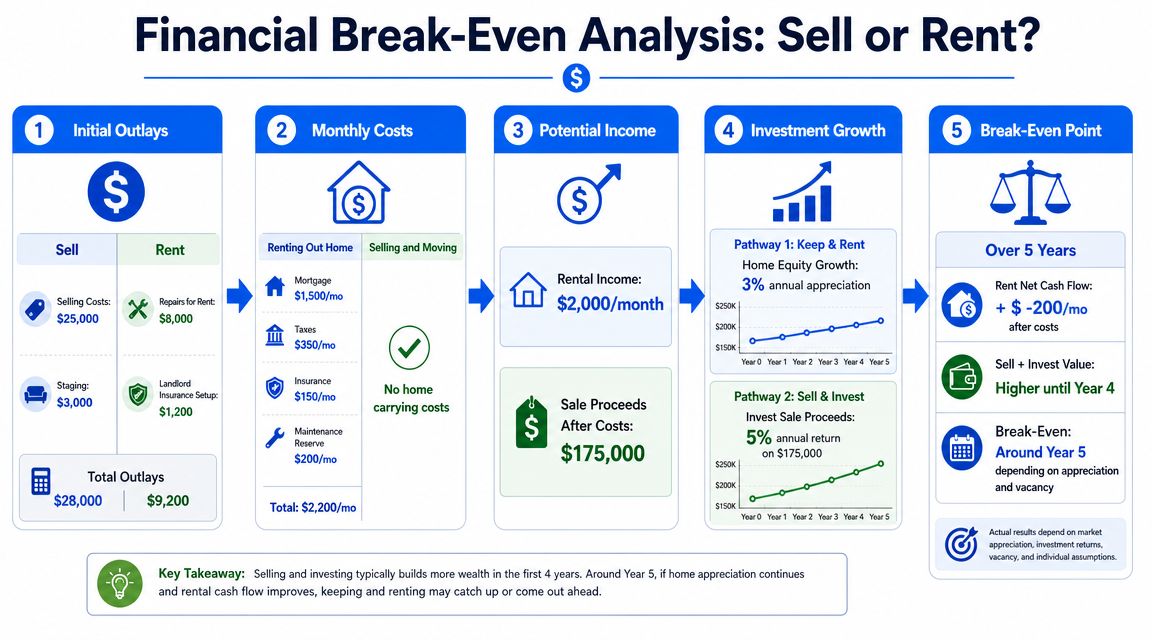

Running the Numbers A Financial Break-Even Analysis

A homeowner leaves for a new job, keeps the old house, and tells himself the rent will “cover the mortgage.” Six months later, he has one vacancy, one repair bill, and a property that ties up cash he needed elsewhere. That is how average decisions get expensive.

Run this like an investor, not a sentimental owner. Selling, renting, and a fast cash sale are three different financial paths. If you do not compare all three with real numbers, you are guessing.

Start with the sale side first

Selling sets the benchmark. Until you know your net cash from a sale today, you cannot judge whether holding the property is worth it.

Calculate these numbers first:

- Net proceeds after closing costs: Estimate what you keep after agent fees, concessions, repairs, and closing expenses.

- Available equity: This is the cash you can use for your next home, debt payoff, emergency reserves, or investing.

- Capital gains treatment: If the home still qualifies as your primary residence, the home sale exclusion can make selling far more attractive than many owners realize.

- Use of proceeds: Money that gets redeployed productively has a job. Money trapped in a weak rental does not.

If you are comparing listing options, include the numbers for a direct sale too. A private sale can reduce transaction costs in some situations, so it is worth reviewing practical alternatives like selling your home privately before assuming a traditional listing is your only clean exit.

Then build the rental case honestly

Now test the hold option with ugly assumptions, not optimistic ones. Rent is the headline number. Cash flow is what matters.

Your rental analysis should include:

- Realistic market rent: Use the rent you can likely achieve, not the best-case asking price you found online.

- Vacancy: Assume the property will sit empty at some point.

- Repairs and maintenance: Former owner-occupied homes usually need more work once they turn into rentals.

- Property management: Even if you self-manage, your time has value.

- Taxes and insurance: These costs keep rising whether the tenant is great or terrible.

- Make-ready costs between tenants: Cleaning, paint, flooring, and minor repairs add up fast.

- Future selling costs: Delaying the sale does not eliminate the exit cost. It postpones it.

- Rental tax treatment: Rental income, depreciation, and recapture change the math in ways many owners underestimate.

A property only earns its keep if it produces durable net cash flow after those costs. If the deal works only with full occupancy, low repairs, and perfect tenants, it does not work.

The break-even question that actually matters

Ask one question: how many years do you need to hold this house before renting beats selling today and putting the proceeds to better use?

That is the main comparison.

The answer depends on financing, tax treatment, expected appreciation, rent growth, and what you would do with the sale proceeds. If you want help framing the tax side of that decision, INTELLI's guide for Texas real estate investors is a useful reference point.

Here is the standard I use. If the home does not create strong monthly cash flow, preserve tax advantages, and still fit your life, sell it. If it needs major repairs, has problem tenants, or you need speed and certainty, compare that result against a fast cash sale too. That third path often wins in distressed situations because it protects time, reduces risk, and turns trapped equity into usable cash now.

Decision test: If your rental math only works when everything goes right, sell the house.

My recommendation on the numbers

Do not keep a property because you hate the idea of “giving up” future appreciation. Appreciation is speculative. Carrying costs are real.

If the property throws off solid net income after realistic expenses, keeping it can make sense. If it barely breaks even, ties up your equity, or creates pressure on your next move, sell it. And if the house needs work, the timeline is tight, or the situation is messy, put a fast cash offer on the same spreadsheet and judge it by net outcome, speed, and hassle avoided.

That is how you make an adult decision. Not by asking whether you can rent it, but by asking which option improves your balance sheet and your life.

The Hidden Realities of Being a Landlord

The phrase “passive income” has done a lot of damage.

Renting out a former home is not passive for most owners. It becomes a legal, operational, and emotional responsibility. You're not just collecting checks. You're running a small housing business, whether you admit it or not.

The spreadsheet misses the ugly parts

A lot of advice focuses on rent and mortgage coverage while skipping operational drag. That's a mistake. As noted in Comerica's discussion of renting versus selling a home, many sell-versus-rent conversations overlook the operational costs of becoming a landlord, especially with tenant-occupied properties. Vacancy risk, eviction exposure, and inheriting a difficult tenant can change the economics fast.

That last point matters more than people realize. If a property already has a tenant in place, you're not buying a clean investment experience. You're inheriting someone else's lease, habits, maintenance expectations, and possibly their conflict history.

Landlord work doesn't wait for your schedule

Here's what owners underestimate:

- Tenant screening: A rushed placement can cost you months of pain.

- Maintenance coordination: The call always comes when you're unavailable.

- Legal compliance: Lease language, notice rules, habitability standards, and local procedures matter.

- Collections and conflict: Good tenants pay. Bad situations consume attention fast.

If you do decide to rent, don't improvise. Learn the basics, tighten your process, and study practical ways to maximize your rental income without cutting corners on tenant quality or operations.

The best tenant makes renting feel easy. The wrong tenant makes you wish you had sold six months earlier.

Tenant-occupied properties are a separate category

I'm especially cautious when a homeowner wants to keep a property that's already occupied. That situation adds friction immediately.

You may face:

- Unclear property condition: Tenants don't always report issues early.

- Lease limitations: Your options are constrained by the agreement already in place.

- Transition headaches: If you later want to sell, a tenant can complicate showings, repairs, and buyer interest.

Homeowners often get trapped. They don't really want a rental business. They just don't want to make a final decision. So they postpone it by becoming a reluctant landlord.

That usually ends badly.

When to Choose a Fast Cash Sale Instead

This is the option most articles bury at the bottom. I won't. For some homeowners, a fast cash sale is the smartest move by far.

Not because it produces the highest price. Usually it doesn't. It wins because it solves the actual problem in front of you: speed, certainty, condition, legal complexity, or plain exhaustion.

Situations where a fast cash sale makes sense

A direct sale is worth serious consideration when one or more of these are true:

- You need to relocate quickly: Waiting through listing prep, showings, and financing contingencies may not fit your timeline.

- The home needs heavy work: A distressed house can scare off financed buyers or force you into repair spending you don't want.

- You inherited a problem property: Probate, deferred maintenance, or leftover belongings can turn a normal sale into a drawn-out mess.

- You're done being a landlord: If you're tired of turnover, repairs, and tenant issues, exit cleanly.

- You're facing financial pressure: When carrying costs are hurting you, time is not your friend.

Why this path works in distressed situations

The benchmark for a rental is not whether the rent covers the mortgage. It's whether gross rent covers all carrying costs, including insurance, property taxes, and other ownership costs, as explained in Redfin's review of whether to sell or rent your home. Redfin also notes that rental profit is taxed as ordinary income, though expenses and depreciation can help offset that burden.

That matters because distressed owners often fool themselves with incomplete math. They think, “The tenant will cover the payment.” But insurance, taxes, repairs, vacancy, and legal issues don't disappear. They pile on.

My recommendation when urgency is the real issue

If you need certainty more than upside, don't list out of habit. Get direct-sale quotes too.

That doesn't mean you must accept one. It means you should compare the certainty of an as-is offer against the delays, prep costs, and risk of a traditional sale. For owners who need a quick exit, one practical option is to review services that buy homes for cash. That route is often most useful when the property is distressed, tenant-occupied, inherited, or tied to a deadline.

A fast sale is not a “lesser” choice when speed and simplicity are the priority. It's a different tool for a different problem.

If you're trying to sell home or rent it out, and the property already feels like a burden, that's your signal. Don't force a hold strategy onto a house that's draining your time and money.

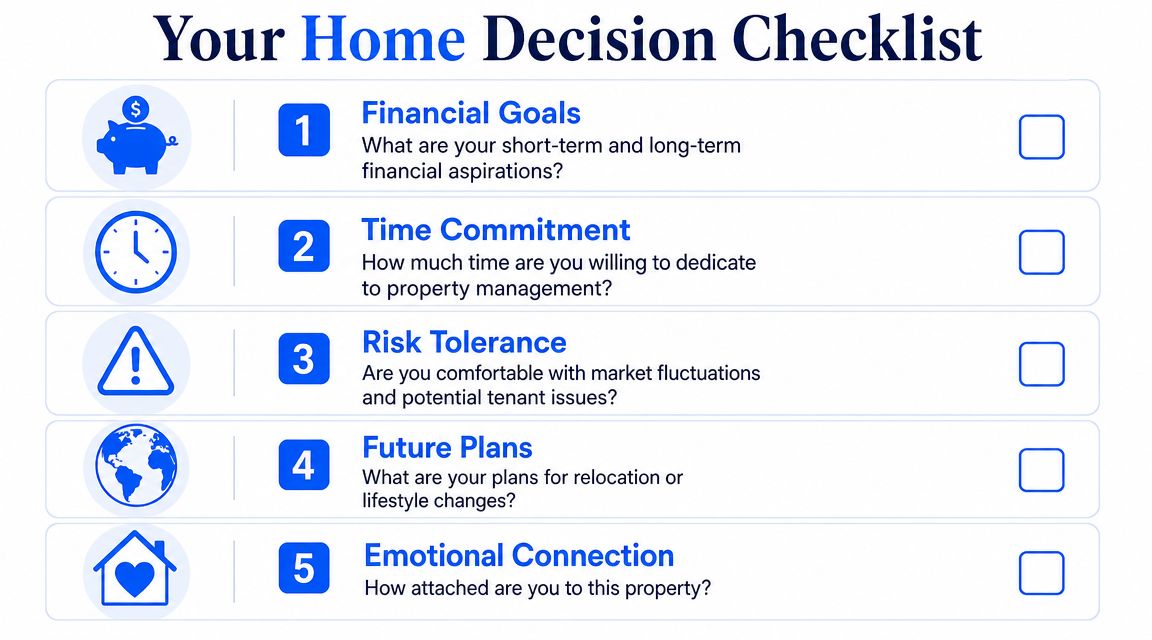

Your Decision Checklist and Clear Next Steps

You're standing in the kitchen, looking at a house you no longer want to manage, and three paths are in front of you. List it. Keep it and become a landlord. Or take the faster exit and sell as-is for cash.

This decision gets easier once you stop treating it like a debate and start treating it like a filter. The right choice is the one that fits your money, your timeline, and your tolerance for hassle. Use real assumptions in your spreadsheet, as noted earlier. Include management costs, vacancy, taxes, repairs, reserves, and what you would do with sale proceeds.

Ask yourself these five questions

- Do you need cash now: If this home is tying up money you need for a move, payoff plan, divorce settlement, or inheritance split, selling is usually the right answer.

- Do you want rental responsibilities: Rent checks sound passive. Tenant issues, lease enforcement, repairs, insurance claims, and vacancy are not.

- Can the property produce a real margin: A rental with thin cash flow is one repair away from becoming a bad hold.

- Is the home ready for the retail market: Updated, clean homes usually justify a traditional listing. Dated, damaged, hoarded, inherited, or tenant-occupied homes often point to a direct cash sale.

- What do you want your next year to look like: More simplicity is a legitimate financial goal. If this house is draining your time and attention, count that cost.

The right next move for each path

If renting still makes sense, do this next:

- Get a realistic rent estimate from someone active in your area

- Speak with a property manager before you commit

- Set aside reserves for repairs, vacancy, and turnover before the first tenant moves in

If a traditional sale fits better, do this:

- Interview agents who know your neighborhood

- Price from comparable sales, not your target number

- Do only the repairs and prep work that are likely to improve your net

If a fast cash sale deserves a look, do this:

- Request an as-is offer

- Compare net proceeds, closing timeline, and the risk of the deal falling through

- Choose certainty if the property is distressed or your deadline is tight

That third option matters more than many owners realize. Selling versus renting is not the full decision. A fast cash sale is often the smartest move when the house needs work, the situation is messy, or you want out without months of prep, showings, and renegotiation.

If you're getting ready for any kind of move, reduce the amount you have to sort, pack, store, or throw away. This guide on how to simplify your move with decluttering is especially useful if you're clearing out a long-time family home or inherited property.

The bottom line is simple. Rent only if the home works as a true investment and you are willing to run it like one. Sell traditionally if the property shows well and you have time to wait for the market. Choose a fast cash sale when speed, condition, or complexity matters more than squeezing out the last dollar.

If you need a clean exit, Cyber Homes is one option to consider for an as-is cash sale. The company buys houses directly, can work on a seller's timeline, and avoids commissions, repairs, and showings. That makes it a practical fit for inherited homes, distressed properties, landlord exits, and situations where certainty matters more than a long listing process.