How to Sell a House As Is: A 2026 Step-by-Step Guide

You might be dealing with a house that became a problem faster than you expected. Maybe it needs repairs you can't fund, maybe you're handling an inherited property, maybe you're moving and the home can't wait for a full retail listing. In that spot, most owners don't need theory. They need a clean way to compare options and make a decision they can live with.

How to sell a house as is comes down to one question: what matters most right now, net proceeds, timeline certainty, or effort? You usually can't maximize all three. You can, however, choose the sale path that fits your actual situation instead of chasing advice written for perfect houses and patient sellers.

What Selling a House 'As Is' Really Means

Selling a house as is means you are offering the property in its current condition. You are telling buyers up front that you won't be making repairs or improvements before closing. The home may still be inspected. The buyer may still decide whether the condition works for them. What changes is your position as the seller. You're not promising a polished, move-in-ready product.

That part matters because many owners hear "as is" and assume it means no responsibility at all. That's not how real transactions work. An as-is sale doesn't give anyone permission to hide known problems. It changes the repair expectation, not the need for honesty.

What buyers hear when they see as is

A retail buyer often reads "as is" as a warning. An investor reads it as a pricing and scope question. An iBuyer reads it through a filter of eligibility and risk. Same phrase, very different reactions.

That's why the right sale path matters as much as the label itself. In practice, most as-is sellers choose one of three routes:

- MLS listing if they want broad exposure and are willing to deal with showings, inspections, and negotiation friction

- iBuyer if the home fits a fairly narrow box and the seller wants a tech-driven process

- Direct investor sale if the home has condition issues, title complexity, tenant issues, or a deadline that makes certainty more valuable than squeezing for retail

Selling as is isn't a shortcut. It's a trade. You give up part of the upside in exchange for less repair work, less prep, and often a faster path to closing.

The real decision isn't legal. It's strategic

The biggest mistake I see is treating as-is as a marketing phrase instead of a strategy. If your house needs substantial work, the main job is not "list it and hope." The crucial task is matching the property to the buyer type most likely to close without drama.

A dated but functional home might still work on the MLS. A property with major deferred maintenance, inherited paperwork, or problem tenants often needs a buyer who can absorb complexity. That's where this choice becomes practical, not emotional.

Deciding if an As-Is Sale Is Your Best Move

Some sellers choose as-is because they want convenience. Others choose it because they don't have another realistic option. Both are valid.

If you're under pressure, trying to force a retail-style sale can cost more than it saves. Time, contractor coordination, carrying costs, and failed escrows all have a price, even when they don't show up as a line item at the start.

When as is usually makes sense

An as-is sale is often the cleanest path if you're dealing with situations like these:

- Foreclosure pressure: You need a sale path that reduces delays and avoids repair projects you can't finish in time.

- Inherited property: The house may be outdated, full of belongings, or tied up in paperwork and family decisions.

- Relocation: You can't manage contractors and repeated showings from another city.

- Landlord fatigue: The property may be occupied, damaged, or not worth rehabbing before sale.

- Heavy repair needs: Roof issues, HVAC failure, mold concerns, structural problems, or long-deferred maintenance can push a standard buyer out of the deal.

Should you fix anything first

Most owners get stuck here. They know the house needs work, but they don't know whether a repair will improve their bottom line.

Zillow's guidance says as-is sales usually trade at a lower price, but sellers should focus on costly safety items like roofs, HVAC, and mold rather than cosmetic fixes. It also notes that homeowners need a way to judge whether a repair improves net proceeds after contractor costs, time, and carrying costs, as explained in Zillow's guidance on selling a house as is when it needs repairs.

Practical rule: If a repair affects safety, financing, or a buyer's ability to insure the property, it's worth evaluating carefully. If it's mostly cosmetic, don't assume you'll get that money back.

Fresh paint, trendy fixtures, and staging-style upgrades often make owners feel better than they make buyers pay more on a distressed property. Major functional issues are different. If the repair removes a financing blocker or a serious red flag, it may help. If it just makes a rough house look slightly nicer, it often doesn't.

A simple decision filter

Ask these three questions before spending money:

Will this repair expand the buyer pool?

Replacing a failed HVAC system might. Replacing dated countertops usually won't.Can you manage the project without delaying the sale?

A repair with contractor delays can erase its own value.Will the house still be judged as distressed afterward?

If the answer is yes, selective patchwork rarely changes the pricing category.

Inherited homes deserve extra caution here because legal timing can matter more than presentation. If you're dealing with that situation, a plain-English overview of selling estate property before probate Texas can help you understand what paperwork and authority issues may affect the sale.

Choosing as-is isn't giving up. In the right situation, it's the most disciplined decision available.

How to Prepare Your House and Documents

An as-is property doesn't need polish. It needs to be easy to evaluate.

Buyers who purchase homes in rough condition want a clear look at the structure, systems, layout, and access points. If the house is packed wall to wall, smells musty, or has blocked rooms, they assume the unknowns are worse than they can see. That usually puts you at a disadvantage.

Prepare for visibility, not perfection

The standard isn't showroom clean. The standard is clear enough for someone to assess the property without guessing.

Start here:

- Remove personal clutter: Empty out what you can, especially from kitchens, bathrooms, hallways, and utility areas.

- Clear blocked access: Make sure buyers can reach the electrical panel, water heater, HVAC, attic access, garage, and any outbuildings.

- Do a real clean: Trash, food, odors, and stained surfaces distract from the home's actual condition.

- Handle basic exterior upkeep: Cut the grass, remove obvious debris, and make the front entry accessible.

- Box what matters: If you're sorting through years of belongings, practical moving boxes in house kits can make the cleanout less chaotic.

A clean distressed house still looks distressed. That's fine. What it doesn't look like is neglected beyond understanding.

Gather your paperwork early

This part speeds up deals more than sellers expect. A good buyer can move quickly only if the file is clean enough to close.

Useful documents include:

- Deed or vesting document

- Recent mortgage statement

- Property tax information

- Utility account details

- HOA documents if applicable

- Lease agreements if tenants are in place

- Any invoices or records for past repairs

- Probate or estate paperwork if relevant

- Photo ID for all owners

If you're not sure what else to collect, a local prep checklist like this to-do list before selling a house in San Antonio is a useful model even if you're outside that market. The same discipline applies almost everywhere.

Missing paperwork doesn't always kill a deal. It does slow closings, create extra title work, and give uncertain buyers a reason to back away.

Disclosures still matter

Some owners hear "as is" and think the disclosure form becomes optional. It doesn't. If you know about roof leaks, prior flooding, electrical issues, plumbing failures, mold, foundation movement, or other material defects, disclose them truthfully.

That protects you in two ways. First, it reduces the chance of a dispute later. Second, it helps you keep control of the narrative. Buyers are far less reactive when they learn about issues from the seller before inspections instead of after.

A good as-is package is simple. Clean house. Clear access. Organized documents. Straight answers.

Pricing Your Property to Attract Cash Buyers

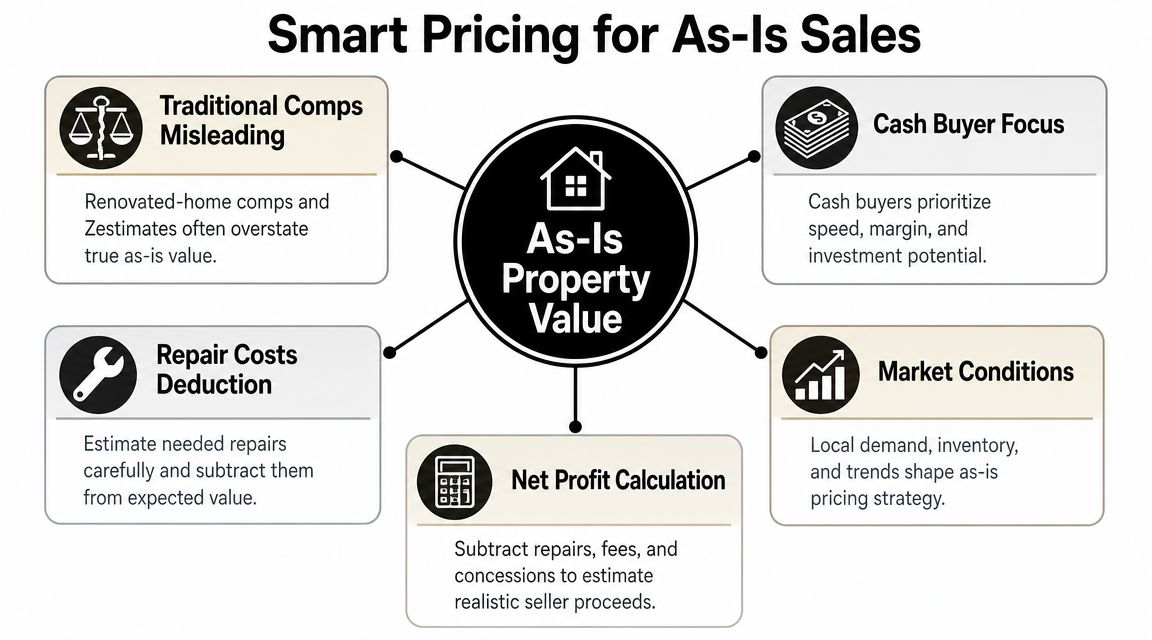

Pricing is where as-is sales succeed or stall. If the number is wrong, nothing else works.

Most owners start with the wrong reference point. They look at renovated comps, online estimates, or the nicest sale nearby and then subtract a little for condition. That's usually not enough. A serious buyer isn't valuing your property like a finished retail home. They're valuing it from an after-repair-value, or ARV, lens.

The basic formula buyers use

In plain language, many cash buyers think about value like this:

Value if fixed up

minus repair costs

minus holding, resale, and risk costs

equals what they can pay now

That doesn't mean every investor uses the same spreadsheet. It means the logic is consistent. If the house needs more work, creates more uncertainty, or will be harder to resell, the offer moves down.

Why retail comps mislead sellers

A technically sound as-is pricing approach starts with repaired value, then deducts the full repair stack and a risk or holding discount instead of anchoring to polished neighborhood sales. Guidance summarized by Chase also notes that sellers should still do a market analysis, but the biggest mistake with as-is homes is pricing off renovated comparables and underestimating repairs, which can lead to longer market time and repeated cuts. The same guidance points to NAR survey data showing that only about 7% of sellers go the FSBO route, and the typical FSBO home sold for $380,000 versus $435,000 for agent-assisted sales, which highlights how pricing and marketing execution affect proceeds in practice, as noted in this Chase summary of selling a house by owner.

That doesn't mean every owner needs an agent. It means pricing discipline matters, and weak exposure plus wishful pricing is expensive.

A workable pricing method

Use a simple process:

Estimate repaired value

Look at nearby homes that sold in updated condition and are similar in size, layout, and location.Get a repair estimate

Use a contractor, experienced investor, or both. Guessing is where most pricing errors start.Subtract transaction friction

Distressed properties carry uncertainty. Title issues, cleanout, financing problems, and longer hold times all affect what a buyer can pay.Set a number that matches your sale path

If you want cash buyers, your price has to reflect a cash buyer reality.

A valuation tool can help you frame the discussion before you start fielding offers. If you want a reference point, this house value estimate tool is one way to start comparing your home's likely as-is position against the broader market.

If several serious buyers say the same repair number range, listen to that signal. Sellers get into trouble when they reject the market's feedback and keep chasing a retail outcome on a non-retail property.

What doesn't work

Three pricing habits almost always create problems:

- Pricing off emotion: What you need from the sale and what the property supports are separate issues.

- Ignoring deferred maintenance: Buyers will find it, and they'll price it in.

- Starting high to leave room to negotiate: In distressed sales, that often scares off the strongest buyers before the conversation starts.

An as-is price should feel a little uncomfortable to the seller. That's usually a sign it's realistic.

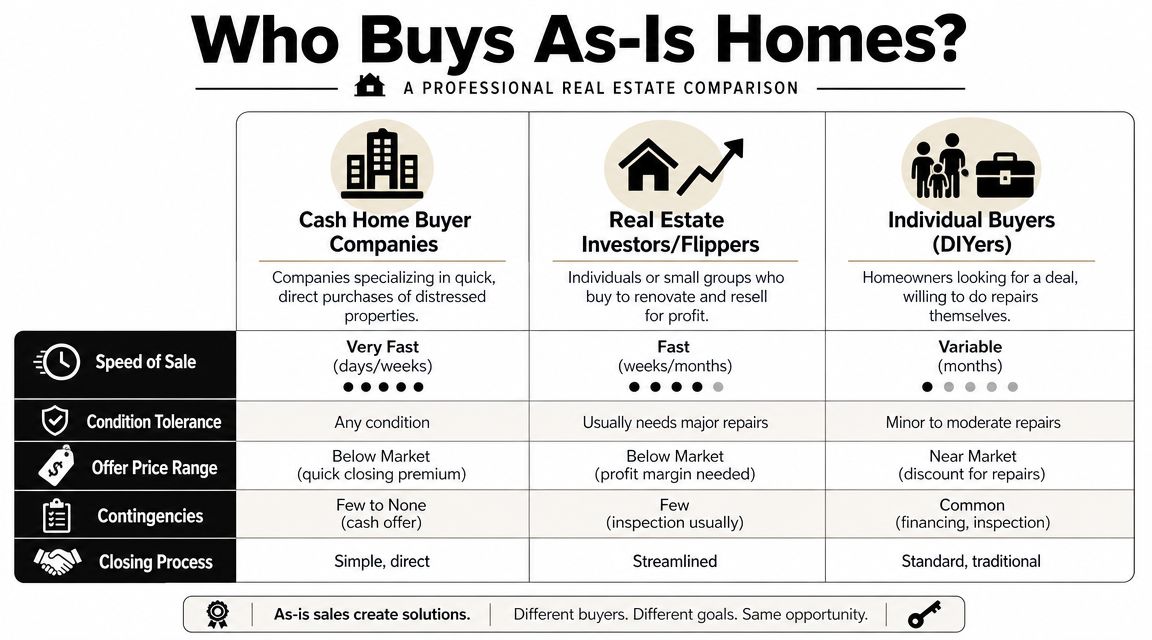

Finding the Right Buyer for Your As-Is Home

Not all buyers solve the same problem. A seller with time, cash for cleanup, and a basically financeable home can choose differently than a seller dealing with mold, probate, liens, or tenants. The right buyer is the one whose process matches your property and your deadline.

This comparison helps.

Side by side comparison

| Buyer path | Best fit | Main upside | Main risk |

|---|---|---|---|

| MLS buyer | Homes in decent enough shape for broad marketing | Highest potential ceiling | More contingencies, repair pushback, slower process |

| iBuyer | Cleaner, more standardized homes in eligible areas | Streamlined experience | Limited condition tolerance and narrower fit |

| Direct investor | Distressed homes, inherited property, rentals, urgent timelines | Speed and certainty | Offer will usually be below retail value |

MLS buyers

Listing on the MLS gives you the widest exposure. If the house is dated but still livable, this route can produce stronger price competition than a direct investor sale. It also makes sense when you have time to prepare the home, manage showings, and absorb negotiation cycles.

The downside is friction. Traditional buyers often need financing. Lenders and appraisers may react badly to serious condition issues. Even if you list as is, many retail buyers still ask for credits, repairs, or price reductions once inspections come back.

This path works best when the house is rough around the edges, not fundamentally troubled.

iBuyers

An iBuyer can be a middle option for sellers who want convenience but have a property that still fits a fairly standard model. The process is usually more systemized than selling to an individual buyer.

The catch is that iBuyers often don't suit homes with major repairs, unusual title issues, or messy occupancy situations. If the property falls outside their comfort zone, the offer may be revised heavily or the home may not qualify at all.

So for true as-is sellers, iBuyers are worth checking, but not assuming.

A short explainer can help if you're comparing direct-sale mechanics. This overview of how to sell your house to an investor in San Antonio lays out the investor route in practical terms.

To see how experienced sellers think through these routes, this quick video is useful:

Direct investors and cash home buyers

Direct investors are usually the best fit when the property itself is the problem. That includes heavy repairs, inherited clutter, title snags, hoarder conditions, tenant complications, or a deadline that makes certainty more important than maximum list price.

Sundae notes that a traditional sale can take 60-90 days, while cash purchases of properties needing work are often completed in roughly seven to 30 days, which is one reason stressed sellers choose that route, according to this Sundae article on selling a house that needs work.

That speed doesn't mean every cash buyer is equal. Some are direct buyers. Some are wholesalers trying to assign the contract. Some have money lined up. Some don't.

How to vet a cash buyer

Before signing anything, ask direct questions:

- Ask for proof of funds: A serious buyer should be able to show they can close.

- Confirm who is buying: If they're wholesaling, ask whether they can assign the contract.

- Read reviews and testimonials: Look for consistency and whether sellers mention follow-through.

- Ask about earnest money: You want to know what happens if the buyer backs out.

- Clarify inspection terms: "As is" should not turn into a wide-open renegotiation window.

One example of a direct-buy option is Cyber Homes, a family-owned investment company that buys houses for cash, purchases properties as-is, and closes through title companies on the seller's timeline. That kind of model is different from listing on the MLS or using a large iBuyer because the focus is on certainty and condition tolerance, not retail exposure.

A simple choice framework

Choose the path that matches your top priority:

- Want the highest possible upside and can tolerate uncertainty? MLS is usually the first look.

- Want a straightforward sale and your home is fairly standard? Check iBuyer eligibility.

- Need speed, fewer contingencies, and a buyer who accepts real problems? Direct investor sales usually fit best.

If you're in a tough spot, certainty often beats theoretical top dollar that never closes.

Navigating the Offer and Closing Process

An as-is offer is more than a price. The terms determine whether the sale is smooth or painful.

I've seen sellers accept the highest number on paper, only to lose weeks to inspection demands, financing trouble, or a buyer who never had the ability to close. A slightly lower offer with cleaner terms can leave you with a better outcome and a lot less risk.

What to look at in an offer

Review these points before focusing on the headline number:

- Cash or financing: Cash usually reduces moving parts.

- Inspection contingency: Is it short and limited, or broad enough to reopen the whole deal?

- Closing date: Can the buyer close when you need to close?

- Earnest money: Is there a meaningful deposit behind the promise?

- Assignment language: If the buyer can assign, understand what that means.

- Occupancy terms: If you need extra time after closing, get it in writing.

The cleanest as-is offers are usually the easiest to live with. Less back-and-forth often matters more than squeezing for one last concession.

What happens after acceptance

Once you sign, the file usually moves to a title company or closing attorney, depending on the state. They verify ownership, check for liens, prepare closing documents, and make sure the legal transfer can happen cleanly.

If there are issues, they surface. Common examples include old mortgages that weren't released properly, unpaid taxes, probate authority questions, divorce-related signature problems, or contractor liens. None of those automatically kills the sale, but each can affect timing.

Seller costs to expect

Even in a straightforward as-is sale, sellers should expect standard transaction items such as:

- Prorated property taxes

- Lien or mortgage payoff

- Title-related charges depending on local custom

- HOA balances if applicable

- Any agreed credits in the contract

The exact split depends on your state and your contract. What matters is seeing the draft settlement statement early enough to ask questions.

Closing day is simpler than most sellers expect

At closing, you'll sign the deed and final settlement documents. The title company or attorney will collect funds from the buyer, pay off any liens that need to be cleared, and then send the remaining proceeds to you, often by wire.

Bring identification. Confirm the wire instructions carefully. Read the settlement statement before signing.

If you've prepared your documents well and chosen a buyer whose process fits the property, closing an as-is deal is usually less dramatic than people fear. The stress almost always comes from misaligned expectations at the beginning, not from the paperwork at the end.

If you need a straightforward as-is sale, Cyber Homes is one option to consider. The company buys houses for cash in their current condition, works through title companies, and lets sellers choose a closing timeline that fits their situation. That can be useful if you're dealing with repairs, probate, relocation, tenants, or a deadline and want to compare a direct sale against listing on the market.